Let’s starts with an example. {Don’t be sentimental, please take it as an example only}

When my grandfather went to the market to buy something, most of the FMCG products were available from Hindustan Unilever. So, my grandfather thought that the company would go very far. He invests in that company and left those equities for me. Now with my great luck, the Hindustan Unilever Company becomes no. 1 in FMCG and I got a huge profit from it. But the twist came here. In my time, Baba Ramdev came in the FMCG sector. In the name of Ayurveda and Swadeshi, He distracts the business of Hindustan Unilever. Now I have two questions.

1) If I leave this Hindustan Unilever Stocks for my grandkids, will the company still perform?

2) May it be possible that Hindustan Unilever may shut down?

It may possible that this company will perform well and give us an extraordinary return. But there is no guarantee about the returns. My Grandfather was right at his end. But I want to tell you that investing in any individual company for the long term is not a wise decision.

Twist One: Where to invest?

Now assume that if my grandfather had the choice to invest in a self-managed portfolio that automatically (right… automatically) removes the non-performing companies and includes the performing one. This portfolio is called Nifty50.

Nifty is NSE’s Index that holds top 50 companies in it. Nifty is a self-managed portfolio and it removes the non-performing companies from it and includes the performing one. It also gave higher weight to the top-performing companies. The more a company performs, the more weight it gains in the portfolio. That means I don’t need to worry about the fundamental or technical analysis. If my grandfather invested in Nifty50, he got the top 50 companies of his time. When he passed that portfolio to me, I will get the top 50 companies of my time and when I will pass that to my grandkids, they will get the top 50 companies of their time.

I know you are arguing that Nifty may also fall, and we may also get loss in it. Wait… There is a solution and there are some more twists

Twist Two: How to secure my capital if the market falls?

Yes. I am not denying. Nifty may fall drastically. But we have a solution for it. We can take hedging through Put Option against it. Hedging works like insurance. Whenever market falls Put premium will rise. In the end, it will give us an exact profit as much loss we made in Nifty. The maximum loss will be the premium of Put Option we paid initially. Other Indian stocks and indices have options with only 3 months expiries while nifty is having options with 5 years expiries. Though liquidity is available only in options of max 1-year expiries.

Surprisingly 1-year ATM Put option in Nifty is trading around 5% of Nifty. That means If I buy Nifty at Rs 10,000 then I need to pay only Rs 500 for the hedging of 1 year. The other will get nifty at Rs. 10,000 but I will buy at Rs. 10500. I will pay an extra 500 but that will ensure me that my maximum loss will be only Rs. 500 if Nifty falls drastically during that year. That means If I invest Rs. 1 crore in this strategy, my 95 lacs will be secure in any worst scenario of Nifty.

Now, this is a good talk. What will be the worst-case scenario?

For example, if nifty is running around 10000 in 2019 and in 2023 nifty will be the same at 10000. That means our loss will be 5% every year. Then you will say it is not a good strategy. Let’s check.

We take a hypothetical scenario in the above table so that we can understand the importance of hedging. We invest Rs. 1 Crore in 2019 and take hedging of Rs 5 lacs to protect that 1 Crore. Now when the market moves to 12000 in 2020 my portfolio will rise to Rs 1.2 crore. Here we will take other insurance for next year and we will pay Rs 6 lacs for that. Now when nifty falls to 8000 in 2021 our portfolio remains the same Rs 1.2 Crore because the loss will be covered from the profit of hedging and we will reinvest it to the nifty. Now when the market starts rising from 8000, we will start earnings from Rs 1.2 Crore and in 2022 when Nifty reaches 12000 our portfolio value will be reached to Rs. 1.8 Crore. Now again if nifty falls to 10000 in 2023, our portfolio remains the same at Rs. 1.8 Crore. Now if we reduce the cost of hedging, we paid every year, our portfolio value will be Rs. 1.54 Crore.

This means that … when Nifty rise our portfolio value rise & when Nifty falls then our portfolio value remains the same. Just think … only this line can help you to achieve your financial freedom.

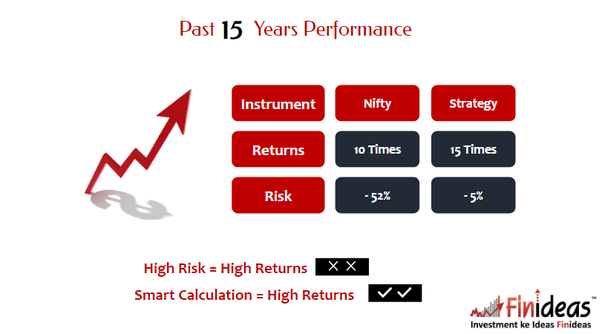

Now above is a hypothetical scenario. What happened in real? Here is the past 15 years of performance.