New ideation-stage startups are exciting, but often they overlook the critical aspect of market research. Market research is the systematic gathering and analysis of data about buyers and the market, providing inferences about the target market, competition, and industry dynamics, crucial for sustainable growth and profitability. By employing techniques such as surveys, focus groups, and data analysis, startups can collect valuable feedback to guide their decisions, ensuring that their offerings align with customer needs.

Effective Market Strategies:

Understanding the Target Market: It helps startups determine optimal pricing, distribution channels, and effective marketing strategies, enhancing customer satisfaction and loyalty.

Validating Business Ideas: Market research reduces the risk of failure and increases the chances of building a feasible and profitable business model.

Investor Appeal: Solid market research enhances by demonstrating an understanding of the market and readiness for success.

Comprehensive Market Research: provides insights into competitor strategies, pricing, and customer engagement, aiding in developing competitive advantages and refining value propositions.

Informed Decisions: It enables data-driven decisions, reduces reliance on intuition, and identifies potential roadblocks and market saturation to mitigate risks.

Better Product Development and Positioning: Market research aids in aligning offerings with customer desires, ensuring a competitive edge through continual improvement.

For better understanding, here are some real-life scenarios like Tune In Hook Up, a video dating site that struggled with traffic. Market research revealed a need for easy video sharing, leading to its rebranding as YouTube. In another instance, Odeo, a podcast platform by Evan Williams and Biz Stone, faced competition from Apple. Insights from market research on user dissatisfaction with content-sharing platforms led to its transformation into Twitter, focusing on simplicity and real-time updates, achieving massive success.

Thereby in the dynamic business world having conducted strong market research becomes indispensable for startups and they can make informed decisions, adapt to changing market trends, and ultimately carve out their place in the competitive landscape, ensuring long-term sustainability and growth.

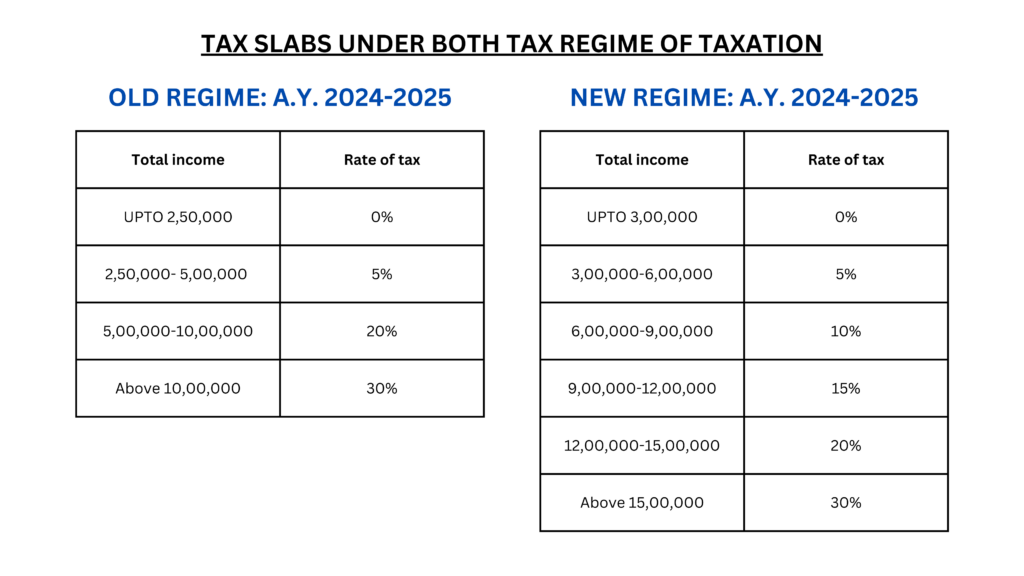

The tax system that existed before the implementation of the new regime is the old tax regime. To design an efficient salary structure and pay minimal tax, employees has an option to choose between the old and new tax regime every financial year.

Benefits of opting for new tax regime:

If Employees are having a total income up to Rs. 7,50,000/- (after claiming standard deduction of Rs. 50,000/- and rebate u/s 87A of Rs. 25,000) which becomes the tax-free income threshold under the new regime, it makes practical sense for employees earning up to 7.5 lakhs to explore the benefits of the new tax regime where the employees does not have any deductions or allowances available to claim

Lower surcharge rate is offered under new tax regime i.e. 25% as compare to old tax regime i.e. 37% for income slab of Rs. 5 crores & above.

Deductions/exemptions available under old regime but will not be available in new regime are:

Interest on home loan (self-owned) [maximum deduction=Rs.2,00,000]

Professional tax

House Rent Allowance ( HRA )

Leave Travel Allowance ( LTA )

Deduction on health insurance premium u/s 80D

Deduction u/s 80C

Employee’s own contributions to NPS account u/s 80CCD(2B)

Exemptions for free food and beverages through vouchers / food coupons

Deduction u/s 80TTA interest on deposits in saving account

Deduction u/s 80TTB interest on deposits with a banking company ( for senior citizens)

Deduction u/s 80CCH

But what if employees are having a total income of more than 7,50,000/- ?

For employees with an income exceeding Rs. 7.5 lakhs, the decision of which tax regime to opt for requires careful consideration of various factors and would depend upon case to case. Now, if the total income is more than Rs. 7,50,000/- there are certain allowances and deductions (other than standard deduction and rebate) which are available only in old tax regime and the employee can claim the benefit of the same and increase their breakeven threshold of paying NIL tax.

CONCLUSION:

Both the old and new tax regimes possess advantages and disadvantages. The previous tax structure encourages taxpayers to cultivate a habit of saving, while the new tax structure favors employees with lower earnings and investments, resulting in fewer deductions and exemptions. However, due to the unique nature of individual deductions and exemptions, a thorough comparison of the two regimes is necessary to determine the best fit for each person. The new income tax regime is designed to accommodate those who prefer minimal deductions or wish to avoid the burden of extensive tax preparation. This includes non-salaried taxpayers, such as consultants, who are not eligible for Section VIA exemptions and deductions. Conversely, senior citizens, who derive a substantial portion of their income from interest, can benefit from the newly introduced Section 80TTB, which allows them to claim Rs.50,000 as interest income deduction. Therefore, they may feel more secure under the old tax regime.

Three Things are permanent in life: Death, Taxes and Surprises in Indian Elections. After 7 phases, 6 weeks and around 640 million votes counted, the world’s largest democracy threw some big surprises. Meanwhile, the Indian stock markets also reacted to each and every happening of the Election Phase; be it the Exit Polls, vote counting or the final results. Let’s dive deeper into understanding the implications of elections on the markets and economy as a whole.

Changes in governments or political parties and ideologies can cause changes in government policies, economic priorities, and regulations, affecting various sectors and companies. While elections create short-term volatility, the long-term effects are mostly shaped by the economic reforms and policies implemented by the ruling party. So, it has been seen that the markets react positively when it is likely to be certain that the ruling party will continue for the next term as well.

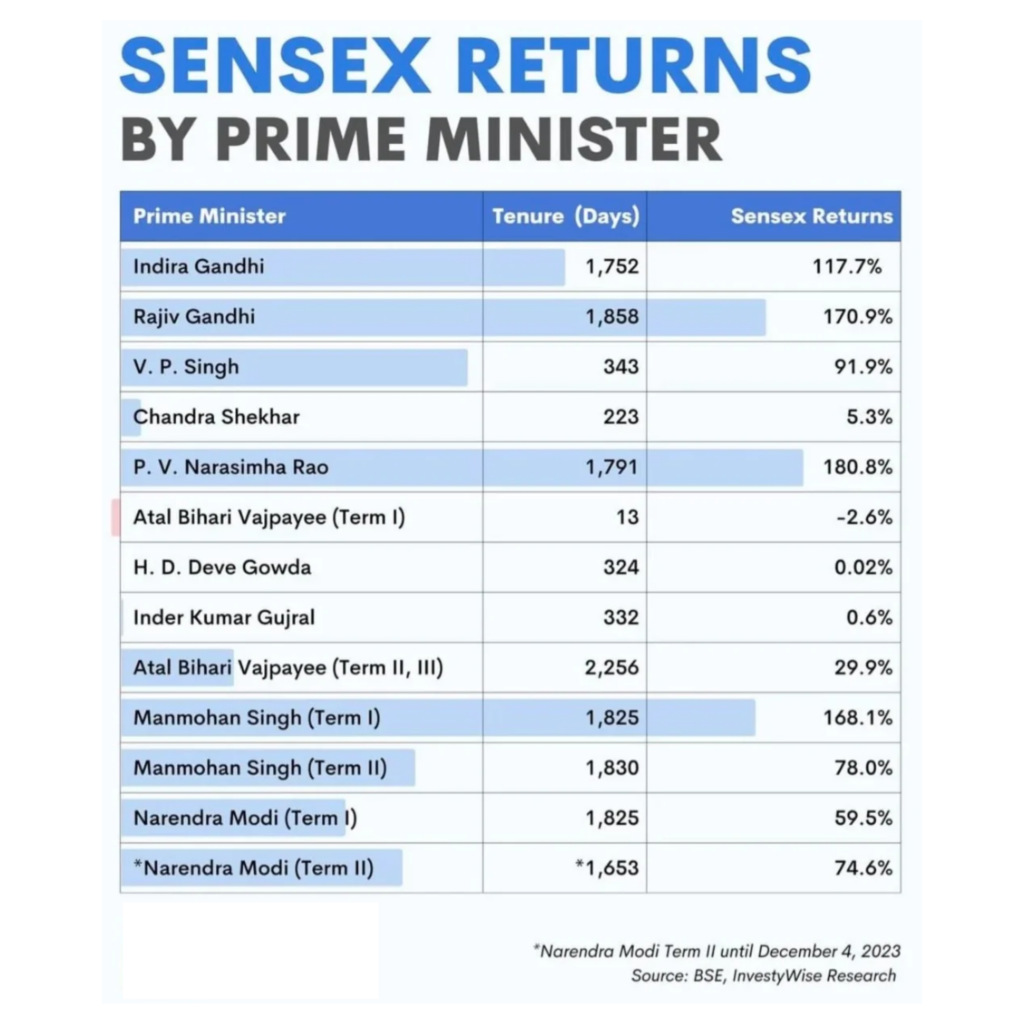

Now, let us take a look at the history, how did the Indian Benchmark Index Sensex fare in the tenure of different Prime Ministers:

Retail investors, often exhibit herd behavior, following trends rather than conducting a thorough analysis. So, they react to every event that may potentially affect the markets. For example, if a contesting party promises to slash tax rates in their election manifesto and the majority of its policies are directed towards economic development, the likelihood of its win might lead to a rise in stock prices. Similarly, if a party with vague and unclear promises shows signs of winning the election, it will create negative market sentiments and lead to a plunge in share prices.

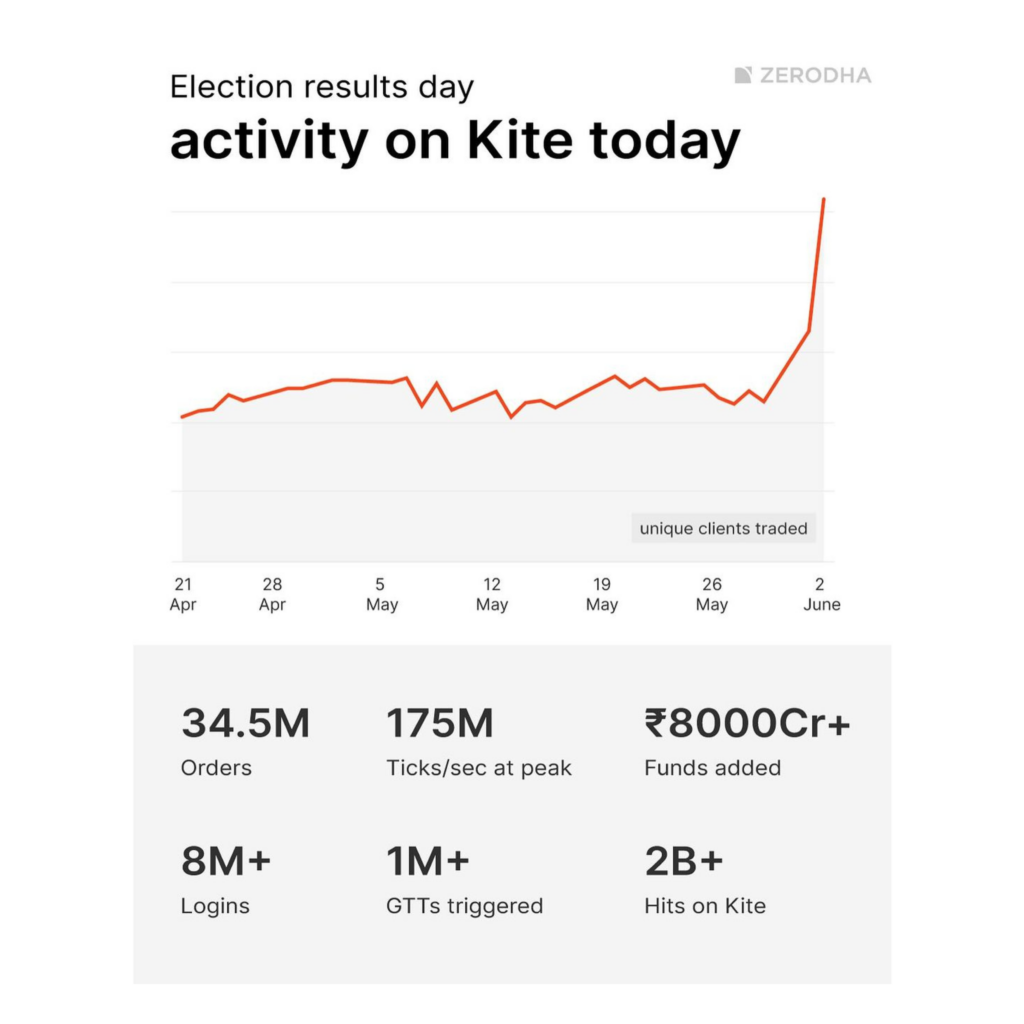

Let’s have a quick look at the recent scenario in the stock market amidst the Lok Sabha Elections. After the conclusion of the elections on 1st June, the exit polls were declared by various media agencies on 2nd June. The exit polls predicted a clear victory for NDA with around 370-380 seats and they were on the track to their “400 Paar” slogan. Reacting to the same, Nifty 50 opened at a gap-up on the following day and touched its all-time high, and also the Nifty PSE Index gained around 8%. Simultaneously, all other indices also celebrated the possible victory of the NDA.

However, on the result day, as the counting of votes started, the result did not meet expectations which led to a bloodbath in the entire market on 4th June with Nifty 50 falling around 6%. However, this did not last long as the markets rebounded very quickly post-results as the final result was the same as the market expected though the seats were fewer (Remember: a win is always a win)

In conclusion, it is clear that the market is made up of the sentiments of lots of retail investors and is very sensitive towards each and every thing affecting the economy. However, the overall ‘India Growth Story’ is still prevalent and it seems that the market will continue its uptrend in the days to come. So, continue to grab the opportunities when the markets dip and keep holding fundamentally sound stocks.

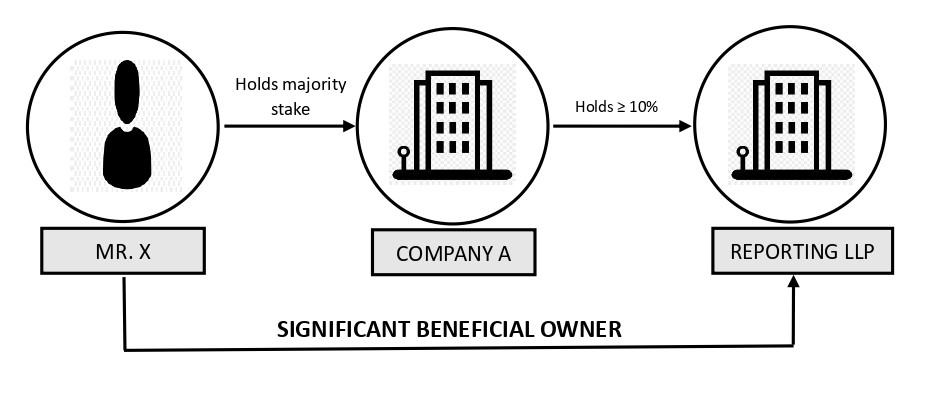

Limited Liability Partnerships (LLPs) are now required to adhere to new compliance measures involving Significant Beneficial Owners (SBOs). A “reporting LLP” refers to a limited liability partnership required to comply with the requirements of section 90 of the Companies Act, 2013, as modified by the notification. An SBO, in relation to a reporting LLP, is an individual, who acting alone or together or through one or more persons or trusts, holds indirectly or together with any direct holdings at least ten percent of the contribution, voting rights, or distributable profit. They are the crucial players who shape the direction and decisions of the LLP.

For Example: If Mr. X holds shares of more than 50% in A Limited and A Limited holds more than 10% voting rights in the reporting LLP, then Mr. X is exercising Significant Beneficial Ownership in the reporting LLP. The graphical presentation of the above example is as follows:

Compliance Steps

The Limited Liability Partnership (LLP) must take necessary steps to identify any individuals who are significant beneficial owners in its structure.

If an individual is identified as a significant beneficial owner, they must provide a declaration in Form No. LLP BEN-1 to the reporting LLP.

Upon receiving the declaration from the significant beneficial owner(s), the LLP must submit the information to the Registrar in Form No. LLP BEN-2 within 30 days of receiving the declaration.

The LLP shall maintain a register of significant beneficial owners in Form No. LLP BEN-3.

The LLP shall issue a notice in Form No. LLP BEN-4, seeking information in accordance with sub-section (5) of section 90, as applied to LLPs by the relevant notification.

Impacts of SBO Declaration:

SBO declarations have profound impacts on promoting transparency, influencing corporate governance, enabling comprehensive disclosures, and reinforcing compliance. It helps to understand the actual individuals who control or benefit significantly from the firm, promoting better decision-making and accountability. The SBO declaration is not merely a regulatory checkbox but a legal mandate. Non-compliance could lead to penalties, reinforcing the integrity of the financial system.

The extension aligns LLPs’ SBO framework with that of companies, aiming to expose complex networks used to conceal ownership. This combats money laundering and terrorism financing. SBO declarations play a crucial role in preventing financial crimes, acting as a deterrent and enabling early intervention.

In conclusion, embracing Significant Beneficial Owner declarations isn’t just a regulatory necessity; it’s a shared commitment to fostering transparent, accountable, and responsible business environments. By navigating the seas of compliance, LLPs contribute to a stronger financial ecosystem, reinforcing integrity and trust.

No travel agency will take you to this route but here’s how we travelled Switzerland with 25+ cities in 11 Days including 4 Boat Cruises for a total price of Rs. 90,000 for family of 2 Adults and 2 Kids using the Swiss Travel System.

Swiss Travel Pass gives you access to unlimited travel by Trains, Trams, buses, and Boats and selected Cogwheel railway too, and entry to 500+ museums.

We bought 2 Adults 15 days Pass for 45k each and we got a Family Card for Free which gives free travel to children less than 16 years and includes free access to excursions like Titlis, and Glacier 3000 too with a paying adult.

Tip: Download the SBB app from the Playstore/ Apple store.

Travel agencies will not suggest this as they have to accommodate a bigger group so they cannot risk one person being late or missing the train.

But the beauty of Swiss Travel is that they are most punctual, are at regular intervals, and are designed meticulously so that interconnecting trains are almost waiting for you on opposite platforms.

Switzerland Day 1-

We selected Lausanne as the Base city for 3 days.

We went to Zermatt which is a beautiful car-free city and you will find beautiful Chalets all around.

Additionally, you can either visit Matterhorn ( Toblerone mountain), or Gornergrat but I would recommend Gornergrat as here, the train will pass through the snow-clad mountains which will be an additional 29 CHF two-way with a 50% discount due to the Swiss Pass.

Day 2 –

We went to Gstaad which is a resort town for celebrities alongside cities of Zweisimmen and Saanen.

In 1995, Dilwale Dulhania Le Jayenge happened, and the economy boomed.

Many scenes from DDLJ were shot here and you can easily find the Café “Early Beck”

Zweisimmen is the station where Simran misses her train to Zurich. The kiosk where she buys the cowbell is still there right next to the station

Saanen railway station was the location for the scene in the movie where Raj and Simran wait to catch the next train to Zurich. The bridge next to the station was the location for the “palat” scene.

Tip: You can board a Panoramic Goldenpass train from Montreux which has a more scenic route. Reservation is optional and mostly you will get a seat easily without reservation. So the Swiss Pass covers more than 10+ Panoramic trains as well.

Day 3 –

We went to the Olympic museum in Lausanne wherein the entry ticket of 2k is included for Free on the Swiss Pass.

We also did a 2.5-hour cruise which is again Free with Swiss Pass and walked along the lake towns of Montreux and Vevey along Lake Geneva.

Imagine, all these towns are developed on mountains but so developed that you will find long Trams running at diagonally elevated heights across the mountains.

Day 4 –

It was a Day to change the Base to Mierengen which was a perfect base to explore places near Interlaken. It is 22 min from Interlaken but you can get properties at almost 1/3rd of rates from main tourist areas like Interlaken or Lucerne

On the same day, we also did another Boat cruise from Lake Brienz to Interlaken again Free with a Swiss Pass which according to me is the most beautiful lake with turquoise blue waters in Switzerland amongst Lake Lucerne, Lake Zurich, Lake Geneva, Lake Thun, etc.

Tip: SBB has a unique service to transfer luggage at 12 CHF per luggage from one town to another. Although costly, I would recommend using this if we analyze our per day cost which goes wasted while we checkout from one hotel, change cities, and check in at another hotel, here you will have hands-free while intercity travel so can visit many small towns in between by Hop on – Hop off any train.

Day 5 –

I always felt Jungfrau – the Top of Europe as a bit overrated for the cost of 9k per person so we decided to ascend to a less touristy but much more beautiful mountain Mannlichen.

Männlichen is a mountain in the heart of the Jungfrau Region with a 360° view. It’s one of the best viewpoints for the famous Eiger, Mönch and Jungfrau.

The journey till Interlaken- Lauterbrunnen – Wengen even though Cogwheel train is covered by Swiss Pass We took a Cable Car from Wengen to Mannlichen and then took a Gondola from Mannlichen to Grindelwald and the excursion was opened just today for Summer 2024. The total cost for a family of 4 was just Rs.7000 for two way ride.

This Cable Car has an upgrade option to the Royal Experience with a Balcony seat for only 5 CHF where you seat on the cable car roof in open for a thrilling experience!

Day 6–

We took a train to Capital city Bern which is like one hour from Interlaken.

Many do not consider Bern as travel city in Switzerland but I really liked the cobble-stoned Old town of Bern with boutique shops. We got a second hand shop wherein all good Board Games were at 5 CHF.

You cannot miss the Clock towers and the two main shopping streets of Kramgasse and Gerechtigkeitsgasse are in the center of the Old Town. The UNESCO World Cultural Heritage Site is lined with six kilometers of arcades that invite visitors to enjoy a special kind of shopping experience.

You will find Trams running along the city which is again Free with Swiss Pass.

Day 7–

This is like a Hidden Gem I am going to share!

– Take a Train to Luzern – 1 hour – Take a scenic Boat Cruise to Vitznau from Pier 1 – 1 hour – Board Europe Oldest Cogwheel railway to Mt Rigi – 40 min and behold!

On May 21, 1871, Europe’s first mountain railway departed on its inaugural ascent from Vitznau to Rigi Staffelhöhe – a milestone in the history of Mount Rigi.

Today, Mount Rigi and its cogwheel railways presents itself as a unique mountain railway paradise and all this again included in Swiss Pass without a single penny extra.

Day 7 continued…

Descend from the other side to Zurich via Arth Goldau and visit the iconic Lindt Chocolate Factory!

The children will love the Chocolate Tour at Lindt. You will also love the Lindt Hot Chocolate at Cafe.

This way you save a day by taking two different routes to ascend and descend.

We also visited Zug and Zurich HB. In Zurich, we simply sit in any Tram , go 3 stops and come back or get down if we see anything interesting.

Tip : Book Lindt Chocolate Tour in advance as they have fixed slots. Cost – Rs. 1.5k pp

In Pics : Check out how a 2 Year Old teaching Life Lessions to her 5 month sibling! Thats what travelling gives which schools cannot!

Food options –

Well, we are still 2 Days to go with all your best wishes and many surprises on the way. For those asking for Lunch Options – 1. Lausanne – Shanti – Indian 2. Gstaad – Mango – Indian 3. Bern – Tibis – Pure Vegan – Pay as per weight 4. Zermatt – Golden India – Indian 5. Mereingen – Hotel Sherlock Homes – Run by Indians Made Pure Jain food for us

And as Gujaratis – Ghar ka Khana Thepla, Khichdi Locho, Home made Nachos. We bring vegetables from Coop or Migros and cook one time (also helps to save cost) or manage breakfast.

In Pics : Pure Jain Buffet ,My daughter enjoying first rains after dinner at Shanti restaurant, our Kitchen !

Yes, I love to plan travel as a hobby and always use Public transport as it helps dwell deep into the culture of the city.

I also agree that sometimes overplanning kills the surprise element while you may enjoy going with the flow but I also love to write and share my experience on travel and the response is overwhelming!

Also Kudos to my 3 Siblings; we studied and grew up together and our respective wives; this is our first trip and that too with 6 Kids of Age 5 months to 8 years.

In recent years, India has witnessed a remarkable surge in the startup ecosystem, with Software as a Service (SaaS) companies emerging as frontrunners in driving innovation and growth.

The SaaS sector in India has experienced exceptional growth, fueled by factors such as increasing internet penetration, a burgeoning digital economy, skilled talent, and supportive government policies. With the expansion of cloud computing and Software as a Service models, startups are leveraging technology to offer scalable solutions to businesses across various sectors.

Key Drivers

Growth

Cost Efficiency

SaaS models enable businesses to access software solutions on a subscription basis. Eliminating the need for upfront investments in infrastructure and licensing fees. This approach makes SaaS products more accessible to startups and SMEs.

Scalability

Inherently scalable, allowing businesses to quickly adapt to changing demands. Expand their operations without significant investments in IT infrastructure or resources.

Focus on Innovation

By leveraging technologies such as Artificial Intelligence, Machine Learning, and Data Analytics. These startups are revolutionizing industries ranging from e-commerce and fintech to healthcare and education.

Notable SaaS Examples:

Zoho Corporation: Founded in 1996 by Sridhar Vembu, Zoho Corporation has grown into one of the world’s leading SaaS companies, offering a suite of cloud-based business applications, including CRM, Finance, HR, and collaboration tools. With over 50 million users worldwide, Zoho exemplifies Indian SaaS excellence on the global stage.

Freshworks Inc.: Freshworks, founded by Girish Mathrubootham and Shan Krishnasamy in 2010, has emerged as a global leader in customer engagement software. The company’s suite of products, including Freshdesk, Freshsales, and Freshchat, helps businesses deliver exceptional customer experiences, driving growth and retention.

Khatabook: Khatabook provides digital ledger solutions and other services to increase efficiency and reduce costs for businesses. Additionally, Khatabook has pivoted to new monetization models, including digital lending offerings, indicating its expansion into various financial services.

Postman: Founded by Abhinav Asthana, Abhijit Kane, and Ankit Sobti in 2014, Postman is a collaboration platform for API development, used by over 17 million developers and 500,000 organizations worldwide. The company’s API testing, documentation, and monitoring tools have become indispensable for software development teams globally.

Conclusion:

The booming SaaS startup scene in India showcases the nation’s growing entrepreneurial landscape and tech capabilities. These companies prioritize innovation, scalability, and customer satisfaction, reshaping the global business software landscape. The Indian SaaS sector is poised to lead the next wave of innovation, shaping the future of industries worldwide.

To encourage investment, the Indian government offers tax benefits to reduce individual tax burdens. However, consistent tax revenue is essential for funding development and public services. To ensure minimum tax collection from those claiming deductions, the Finance Act of 1996 introduced Minimum Alternate Tax (MAT) for corporations. Similarly, the Finance Act of 2011 introduced Alternative Minimum Tax (AMT) for non-corporate taxpayers.

What Is AMT, and Why Was It Implemented?

Alternative Minimum Tax is an alternative to the regular tax liability. It does work on the same principle as MAT, but it is unique in terms of applicability, exemptions, rules, deductions, and calculations.

The government introduced AMT in order to find a balance between offering tax deductions/exemptions and collecting minimal taxes.

Applicability of AMT

List of taxpayers covered under Section 115JC of the IT Act:

Non-corporate taxpayers

Individuals, HUFs, Body of Individuals, and Association of Persons (only when their total adjusted income exceeds Rs. 20,00,000 annually)

However, these taxpayers have to pay AMT only when they claim the following deductions:

Deductions claimed under Chapter VI A of IT Act: These include Sections 80H to 80RRB but taxpayers claiming deductions under Section 80P related to cooperative societies are not eligible for paying AMT.

Deductions claimed under Section 35D of the IT Act: This Section allows 100% deductions on depreciation of capital assets when such assets have been in use for some specific businesses like cold storage facilities, fertilizer manufacturing, etc.

Additionally, taxpayers claiming deductions under Section 10AA of the Income Tax Act need to pay AMT.

Tax Liability Applicable for AMT

The tax liability will be higher of the two whenever AMT is applicable under Section115JC of the Income Tax Act:

Tax liability is computed as per normal slab rates after taking into consideration all deductions and relaxations available under different chapters of the IT Act.

Tax liability computed as per AMT rate of 18.5% on adjusted total income.

What is AMT Credit?

A non-corporate taxpayer to whom the provisions of AMT apply has to pay higher of normal tax liability or liability as per the provisions of AMT. If in any year the taxpayer pays liability as per AMT, then he is entitled to claim credit in the subsequent year(s) of AMT paid above the normal tax liability.

The credit can be adjusted in the year in which the liability of the taxpayer as per the normal provisions is more than the AMT liability. The set off in respect brought forward AMT credit shall be allowed in the 15 subsequent year(s) to the extent of the difference between the tax on his total income as per the normal provisions and the liability as per the AMT provisions.

For Example:

F.Y. 2023-24:

Normal Rates = Rs. 12,00,000/-

As per AMT= Rs. 14,00,000/-

Liable to pay AMT as tax liability as per normal rate is lower.

F.Y. 2024-25:

Normal Rates = Rs. 16,00,000/-

As per AMT= Rs. 15,00,000/-

Liable to pay tax as per the normal rates.

As there was AMT paid in the preceding year, they have total AMT credit of Rs. 14,00,000 – Rs. 12,00,00 = Rs. 2,00,000 with them.

They can use this credit for an amount not exceeding the difference between the normal rate and AMT in FY 2024-25 i.e. Rs. 1,00,000 (Rs. 16,00,000 – Rs. 15,00,000). The remaining credit can be forwarded to the coming years.

In India, both startup and MSMEs are eligible for certain tax benefits and exemptions to promote entrepreneurship and economic groups.

Startups (incorporated as a private limited company or registered as a partnership firm or a limited liability partnership, having turnover less than 100cr in any of the previous financial years shall be considered as a startup up to 10 years from the date of incorporation) are newly established businesses, often founded by entrepreneurs aiming to address specific problems or capitalize on market opportunities. Startups are known for their agility, creativity and willingness to take risks.

TAX INCENTIVES FOR STARTUPs

Startups can avail three-year tax holiday under Sec. 80IAC of the Income Tax Act 1961, provided they are recognized by DPIIT and are incorporated between 1st April 2016 to 31st March 2025.

Startups recognized by DPIIT are exempted from angel tax(tax paid by startups on the excess amount received by way of investment when investments exceed its FMV) provided they meet certain criteria.

MSMEs stand for Micro, Small and Medium enterprises. These are the businesses that fall within certain criteria regarding their size, investment in plant and machinery or equipment and annual turnover. MSMEs play a vital role in economic development and job creation.

TAX INCENTIVES FOR MSMEs

MSMEs are eligible for concessional tax rates under section 115BA of the Income Tax Act 1961. Certain domestic companies, including MSMEs, are eligible for a reduced tax of 25% instead of the standard rate of 30% by fulfilling certain conditions.

MSMEs can also opt for a tax rate of 22% under section 115BAA of the Income Tax Act 1961 by fulfilling certain conditions. This section allows domestic companies including MSMEs to calculate the total income without considering certain deductions. This section applies to those companies other than those covered under sec 115BA.

MSMEs may be granted tax holidays during which they are exempt from paying taxes for a specified period, to encourage new business or to promote growth.

MSMEs who are engaged in secondary steel production are now eligible to get an extension of customs duty exemption on steel scrap.

CONCLUSION

Tax exemptions and benefits are instrumental in supporting the growth, innovation and competitiveness of both MSMEs and startups. Leveraging tax benefits and exemptions is vital for the growth and success of startups and MSMEs in India. By utilising these incentives effectively, entrepreneurs can strengthen their financial positions.

In today’s interconnected global economy, entrepreneurs are increasingly expanding their businesses across international borders. However, along with the opportunities come challenges, one of which is navigating the complex realm of taxation. Double taxation, wherein income is taxed in more than one jurisdiction, poses a significant hurdle for businesses operating internationally. This is where Double Taxation Avoidance Agreements (DTAA) come into play, offering a roadmap to mitigate the impact of double taxation and ensure a fair distribution of tax liabilities between countries.

Understanding DTAA:

DTAA, as the name suggests, is an agreement between two countries aimed at avoiding the burden of double taxation on the same income. These agreements lay down the rules regarding the taxation of various types of income, including dividends, interest, royalties, and capital gains, earned by residents of one country in another country. By establishing clear guidelines for taxation, DTAA provides certainty and prevents situations where taxpayers are taxed twice on the same income.

Indian Legalities:

India, acknowledging DTAA’s significance, has inked agreements with many nations to ease cross-border trade and investment. As of 2024, India has signed DTAA agreements with more than 90 countries, including major economies like the United States, United Kingdom, Singapore, and Germany. These agreements vary in their terms and conditions, reflecting the unique bilateral relationships between India and each partner country.

Specific Agreements:

While all DTAA agreements follow a similar framework, some may contain provisions that warrant special attention from users.

For instance, the DTAA between India and Mauritius has historically been of particular significance to investors due to its favorable provisions regarding capital gains taxation. Under this agreement, capital gains derived from the sale of shares by residents of one country in another country are taxed only in the country of residence, providing a significant tax advantage for investors.

Similarly, the DTAA between India and Singapore also offers favorable terms for capital gains taxation, making Singapore an attractive destination for investment by Indian entrepreneurs.

Methods in DTAA:

Under DTAA, there are generally two methods used to relieve taxpayers from the burden of double taxation: Tax Credit and Tax Exemption.

1. Tax Credit:

Tax credit, also known as the credit method, allows taxpayers to offset taxes paid in one country against the tax liability in another country.

Example: Suppose an Indian entrepreneur, Raj, conducts business in the United States and earns income subject to taxation in both India and the U.S. According to the DTAA between India and the U.S., Raj can claim a tax credit in India for the taxes he paid in the U.S. on the same income.

Let’s say Raj’s business in the U.S. generated a profit of $50,000, on which he paid $10,000 in taxes to the U.S. government. Now, when Raj reports this income in India, he can claim a tax credit for the $10,000 already paid to the U.S. This means that Raj’s tax liability in India will be reduced by the amount of tax already paid in the U.S., resulting in a lower overall tax burden.

2. Tax Exemption:

Tax exemption, also known as the exemption method, allows certain types of income to be exempt from taxation in one of the countries involved in the DTAA. Example: Consider an Indian company, XYZ Ltd., which receives dividends from its subsidiary in Germany. Under the DTAA between India and Germany, dividends received by XYZ Ltd. from its German subsidiary may be exempt from taxation in India.

Let’s say XYZ Ltd. receives dividends amounting to €20,000 from its German subsidiary. If this income qualifies for exemption under the DTAA, XYZ Ltd. does not have to pay tax on these dividends in India. Instead, the dividends may only be taxed in Germany, according to German tax laws.

Conclusion:

In conclusion, DTAA plays a pivotal role in facilitating international business activities by providing clarity and certainty in taxation matters. For Indian entrepreneurs venturing into the global market, understanding the implications of DTAA agreements is essential to optimize tax efficiency and avoid the pitfalls of double taxation. By effectively leveraging DTAA agreements, businesses can confidently expand their global presence, assured of fair and transparent tax management.

The Goods and Services Tax (GST) is a comprehensive indirect tax that was implemented in India on 1st July, 2017.

The government of India has undertaken a big taxation reform by introducing GST, which is expected to enhance the growth of E-commerce. GST is a single destination-based indirect tax that is applicable across all states on the supply of goods or services. The CGST Act, under Section 9(5), defines electronic commerce as “the supply of goods or services or both, including digital products, over a digital or electronic network” and defines Electronic Commerce Operator (ECO) as “any person who owns, operates, or manages a digital or electronic facility or platform for electronic commerce.” E-commerce operators like Amazon act as an intermediary and bring buyers and sellers together, and facilitate transactions. ECOs have to mandatorily register for GST regardless of turnover.

“Persons who sell goods or services, or both through an ECO are E-commerce Sellers.”

REGISTRATION REQUIREMENTS FOR E-COMMERCE SELLERS

Type of Activity

Registration Requirement

Selling Goods

Compulsory Registration

Providing Services other than those listed u/s 9(5)

Register only if turnover is more than 10/20 lakhs

Providing Services listed u/s 9(5)

Not required to register

Earlier in the service tax, a centralized system for registration was available,but under the GST a centralized system for registration is not available as the place of supply will decide the scope of registration.

GST is likely to increase costs for the E-commerce industry due to high expenses in storing and warehousing goods. The company have to pay taxes on unsold goods and can only reclaim them upon sale.

FOLLOWING ARE A FEW EXAMPLES OF REGISTRATION REQUIREMENTS OF DIFFERENT INDUSTRIES

Industry

Examples of E-commerce operator

Registration requirement

E-Commerce Sellers (goods)

Amazon, Flipkart

The seller is required to register.

Hotel (turnover less than 10/20 lakh)

OYO, Make My Trip

The hotel is not required to register.

Hotel (turnover of the hotel more than 10/20 lakh)

OYO, Make My Trip

The hotel is required to register.

Previous indirect tax policies created considerable confusion and led to extensive litigation, impeding the growth of the e-commerce sector in India. The lack of clarity resulted in tax evasion, causing substantial revenue losses for the government. The introduction of GST aims to streamline the tax system, close loopholes, and potentially lessen the overall tax burden.

GST has a significant impact on the E-commerce marketplace. The influence of GST on the landscape of Indian e-commerce is unmistakable. With streamlined tax processes, including mechanisms like Tax Collected at Source (TCS) and Input Tax Credit (ITC), GST has forged the path towards uniformity, transparency, and compliance with the e-commerce sector. From mandatory registration to addressing common challenges, navigating GST requirements is critical for e-commerce entities to operate legally and contribute to a fairer tax ecosystem.