The FM has announced New Income Tax Slab for AY 2020-21 giving taxpayers an option to pay taxes as per the new tax slabs.

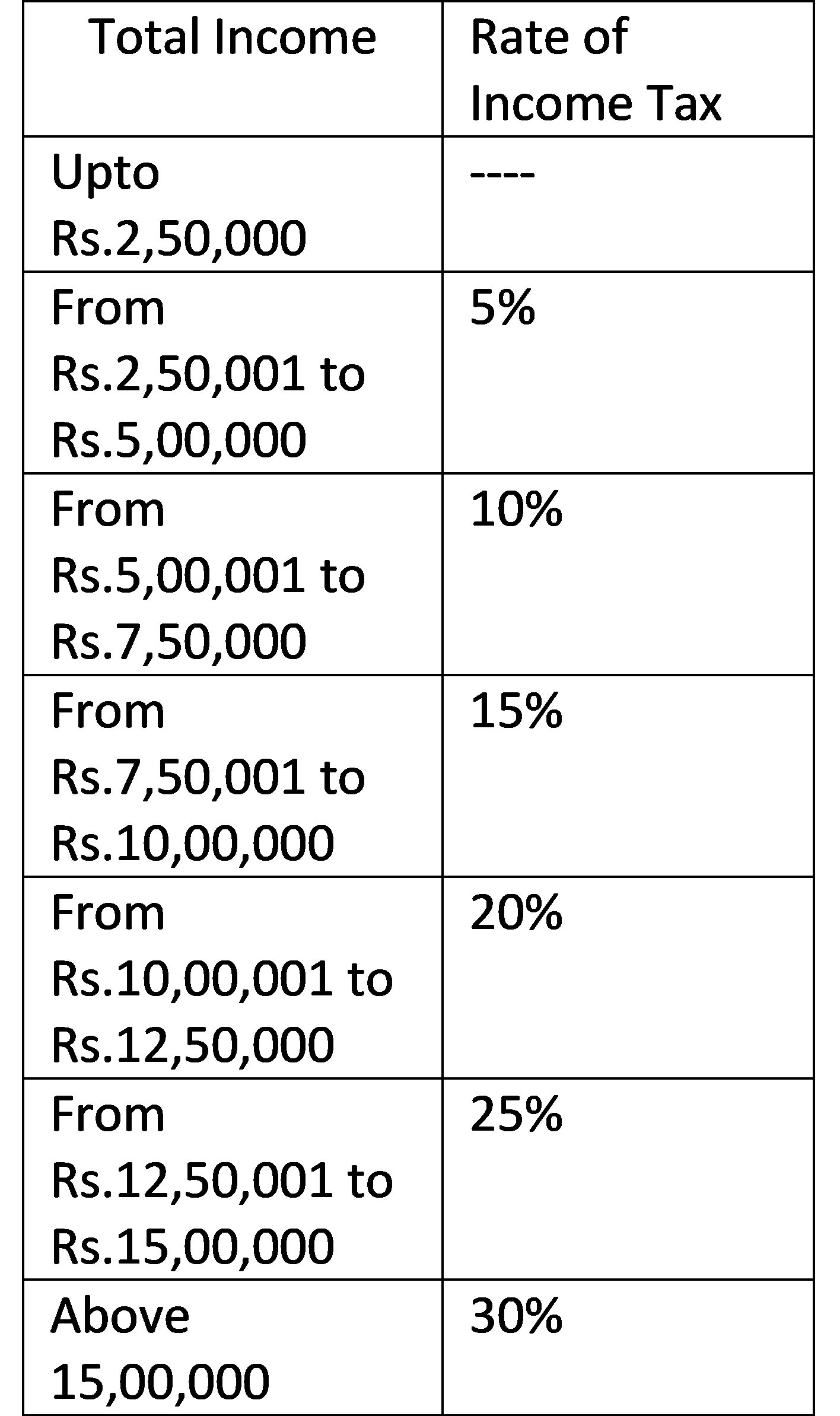

Income Tax Slab for A.Y 2020-21 and 2021-22 for Individuals/HUF

New Income Tax Rate For AY 2020-21 For Individual/HUF

| Entity type | Income Tax Slabs | |

| 1. Individuals/HUF | A.Y.2020-21 | A.Y.2021-22 |

| Individual (other than Senior or super senior citizen) and HUF (Including AOP, BOI and Artificial Juridical Person) |  | |

| Individual -Senior Citizen (who is 60 years or more at any time during the previous year) |  | |

| Individual -Super Senior Citizen (who is 80 years or more at any time during the previous year) |  | |

| Tax rates if the assessee has opted for section 115BAC | ||

| Individuals and HUF [Note: The option to pay tax at lower rates shall be available only if the total income of assessee is computed without claiming specified exemptions or deductions ] | — |  |

Plus: –

Health and Education cess: – 4% of income tax and surcharge.

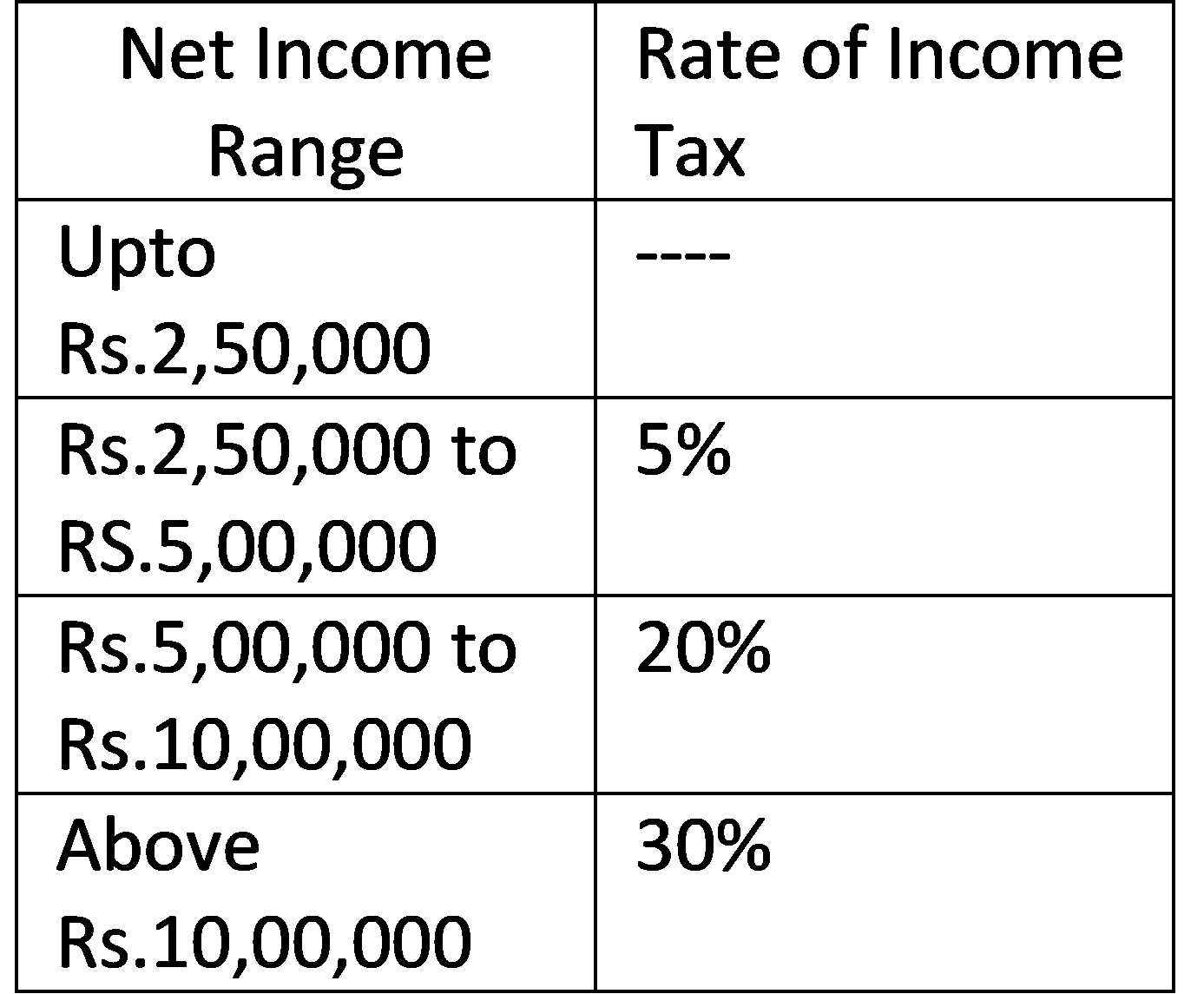

Note: A resident individual (whose net income does not exceed Rs. 5,00,000) can avail rebate under section 87A. It is deductible from income-tax before calculating education cess. The amount of rebate is 100 per cent of income-tax or Rs. 12,500, whichever is less.

Surcharge: – 10% of income tax where total income exceeds Rs. 50,00,000.

15% of income tax where total income exceeds Rs. 1,00,00,000.

25% of income tax where total income exceeds Rs. 2,00,00,000.

37% of income tax where total income exceeds Rs. 5,00,00,000.

Note – Enhanced surcharge levied at the rates of 25%/37% shall not be levied in case of income chargeable to tax under sections 111A, 112A and 115AD. Hence, the maximum rate of surcharge on tax payable on such incomes shall be 15%.

However, marginal relief is available from surcharge in following manner-

| In case where net income | Marginal relief shall be available from surcharge in such a manner that |

| Exceed 50 lakhs but doesn’t exceed Rs. 1 Crore | The amount payable as income tax and surcharge shall not exceed the total amount payable as income tax on total income of Rs 50 Lakh by more than the amount of income that exceeds Rs 50 Lakhs. |

| Exceed 1 Crore but doesn’t exceed Rs. 2 Crore | The amount payable as income tax and surcharge shall not exceed the total amount payable as income-tax on total income of Rs. 1 crore by more than the amount of income that exceeds Rs. 1 crore. |

| Exceed 2 Crore but doesn’t exceed Rs. 5 Crore | The amount payable as income tax and surcharge shall not exceed the total amount payable as income-tax on total income of Rs. 2 crore by more than the amount of income that exceeds Rs. 2 crore. |

| Exceeds Rs. 5 crore | The amount payable as income tax and surcharge shall not exceed the total amount payable as income-tax on total income of Rs. 5 crore by more than the amount of income that exceeds Rs. 5 crore |

New Income Tax Slab For Assessment Year 2020 21 For Firms/LLP

| Entity type | Income Tax Slabs | |

| 2. Firms | A.Y.2020-21 | A.Y.2021-22 |

| Partnership Firm [including LLP] | 30% | 30% |

Plus:-

(a) Health and Education cess: – 4% of income tax and surcharge.

(b) Surcharge : 12% of income tax where total income exceeds Rs.1 Crore.

However, the surcharge shall be subject to marginal relief

| In case where total income | Marginal relief shall be available from surcharge in such a manner that |

| Exceeds Rs. 1 Crore | The total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of one crore rupees by more than the amount of income that exceeds one crore rupees. |

New Income Tax Slab For Assessment Year 2020-21 For Companies

| Entity type | Income Tax Slabs | |

| 3. Domestic Company | A.Y.2020-21 | A.Y.2021-22 |

| Where its total turnover or gross receipt during the previous year 2017-18 does not exceed Rs. 400 crore | 25% | — |

| Where its total turnover or gross receipt during the previous year 2018-19 does not exceed Rs. 400 crore | — | 25% |

| Any other Domestic company | 30% | 30% |

| Special Tax rates applicable to a domestic company | ||

| Where it opted for section 115BA (NOTE 1) | 25% | 25% |

| Where it opted for Section 115BAA (NOTE 2) | 22% | 22% |

| Where it opted for Section 115BAB (NOTE 3) | 15% | 15% |

Note 1: Section 115BA – A domestic company which is registered on or after March 1, 2016 and engaged in the business of manufacture or production of any article or thing and research in relation to (or distribution of) such article or thing manufactured or produced by it and also It is not claiming any deduction u/s 10AA, 32AC, 32AD, 33AB, 33ABA, 35(1)(ii)/(iia)/(iii)/35(2AA)/(2AB), 35AC, 35AD, 35CCC, 35CCD, section 80H to 80TT (Other than 80JJAA) or additional depreciation, can opt section 115BA on or before the due date of return by filing Form 10-IB online. company cannot claim any brought forwarded losses (if such loss is related to the deductions specified in above point).

Note 2: Section 115BAA – Total income of a company is taxable at the rate of 22% (from A.Y 2020-21), if the following conditions are satisfied: – Company is not claiming any deduction u/s 10AA or 32(1)(iia) or 32AD or 33AB or 33ABA or 35(1)(ii)/(iia)/(iii)/35(2AA)/(2AB) or 35AD or 35CCC or 35CCD or section 80H to 80TT (Other than 80JJAA). – Company is not claiming any brought forwarded losses (if such loss is related to the deductions specified in above point). – Provisions of MAT is not applicable on such company after exercising of option. company cannot claim the MAT credit (if any available at the time of exercising of section 115BAA).

Note 3: Section 115BAB – Total income of a company is taxable at the rate of 15% (from A.Y 2020-21), if the following conditions are satisfied:

– Company (not covered in section 115BA and 115BAA) is registered on or after October 1, 2019 and commenced manufacturing on or before 31st March, 2023.

– Company is not formed by splitting up or reconstruction of a business already in existence.

– Company does not use any machinery or plant previously used for any purpose.

– Company does not use any building previously used as a hotel or a convention center, as the case may be.

– Company is not engaged in any business other than the business of manufacture or production of any article or thing and research in relation to (or distribution of) such article or thing manufactured or produced by it. Business of manufacture or production shall not includes business of –

- Development of computer software;

- Mining ;

- Conversion of marble blocks or similar items into slabs;

- Bottling of gas into cylinder;

- Printing of books or production of cinematographic film; or

- Any other notified by Central Govt.

– Company is not claiming any deduction u/s 10AA or 32(1)(iia) or 32AD or 33AB or 33ABA or 35(1)(ii)/(iia)/(iii)/35(2AA)/(2AB) or 35AD or 35CCC or 35CCD or section 80H to 80TT (Other than 80JJAA and 80M).

– Company is not claiming any brought forwarded losses (if such loss is related to the deductions specified in above point).

– Provisions of MAT is not applicable on such company after exercising of option. company cannot claim the MAT credit (if any available at the time of exercising of section 115BAA).

Education Cess: 4% of Income tax plus surcharge

Surcharge:

a) 7% of Income tax where total income exceeds Rs.1 crore

b) 12% of Income tax where total income exceeds Rs.10 crore

c) 10% of income tax where domestic company opted for section 115BAA and 115BAB

However, the surcharge shall be subject to marginal relief for in any other case, which shall be as under:

| In case where total income | Marginal relief shall be available from surcharge in such a manner that |

| Exceed 1 Crore but doesn’t exceed Rs. 10 Crore | The total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of Rs. 1 crore by more than the amount of income that exceeds Rs. 1 crore. |

| Exceeds 10 Crore | The total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of Rs. 10 crore by more than the amount of income that exceeds Rs. 10 crore |

| Entity type | Income Tax Slabs | |

| 4. Foreign Company | A.Y.2020-21 | A.Y.2021-22 |

| Irrespective of Turnover or gross receipts or income | 40% | 40% |

Plus:-

- Health and Education cess: – 4% of income tax and surcharge.

- Surcharge: 2% if income exceed Rs. 1 crore but does not exceed Rs. 10 crore.

5% if income exceeds Rs. 10 crore.

However, the surcharge shall be subject to marginal relief for in any other case, which shall be as under:

Also Read:

| In case where total income | Marginal relief shall be available from surcharge in such a manner that |

| Exceed 1 Crore but doesn’t exceed Rs. 10 Crore | The total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of Rs. 1 crore by more than the amount of income that exceeds Rs. 1 crore. |

| Exceeds 10 Crore | The total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of Rs. 10 crore by more than the amount of income that exceeds Rs. 10 crore |

NewIncome Tax Slab For AY 2020-21 For Local Authority

| Entity type | Income Tax Slabs | |

| 5. Local Authority | A.Y.2020-21 | A.Y.2021-22 |

| Local Authority | 30% | 30% |

Plus:-

- Health and Education cess: – 4% of income tax and surcharge.

- Surcharge: 12% of income tax where total income exceeds Rs. 1 Crore

However, the surcharge shall be subject to marginal relief

| In case where total income | Marginal relief shall be available from surcharge in such a manner that |

| Exceeds Rs. 1 Crore | The total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of one crore rupees by more than the amount of income that exceeds one crore rupees. |

New Income Tax Slab For Assessment Year 2020 21 For Co-operative Society

| Entity type | Income Tax Slabs | |

| 6. Co-operative Society | A.Y.2020-21 | A.Y.2021-22 |

| Co-operative Society |  | |

| Spceial tax regime under section 115BAD | ||

| If the conditions mentioned u/s.115BAD are satisfied | 22% | 22% |

Plus:-

- Health and Education cess: – 4% of income tax and surcharge.

- Surcharge :

In case assessee has opted for section 115BAD:

Flat 10% irrespective of amount of total income

In any other case:

12% of income tax where total income exceeds Rs. 1 Crore

However, the surcharge in any other case shall be subject to marginal relief

| In case where total income | Marginal relief shall be available from surcharge in such a manner that |

| Exceeds Rs. 1 Crore | The total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of one crore rupees by more than the amount of income that exceeds one crore rupees. |